Building a Scalable GenAI Architecture for FinTech Workflows

This guide outlines a robust, modular GenAI architecture tailored for FinTech, enabling secure, scalable AI use across credit, fraud, KYC, and compliance domains.

Join the DZone community and get the full member experience.

Join For FreeGenerative AI (GenAI) is rapidly transforming the financial services landscape. According to McKinsey, GenAI could unlock up to $340 billion in annual cost savings and productivity gains across the global banking sector. With this momentum, forward looking fintech leaders are embedding GenAI into critical workflows ranging from customer onboarding and credit decisioning to fraud detection and compliance. This article provides a practical architecture guide to help technology leaders adopt GenAI safely, effectively, and at scale.

Why GenAI Matters for Financial Services

Financial institutions are under constant pressure to operate faster, smarter, and leaner. GenAI provides a strategic edge by:

- Accelerating decisions in credit, fraud resolution, and customer service.

- Lowering costs by reducing manual effort through automation.

- Improving compliance with explainable AI outputs.

- Enhancing customer experience via intelligent, real time interactions.

How GenAI Fits into FinTech Architecture

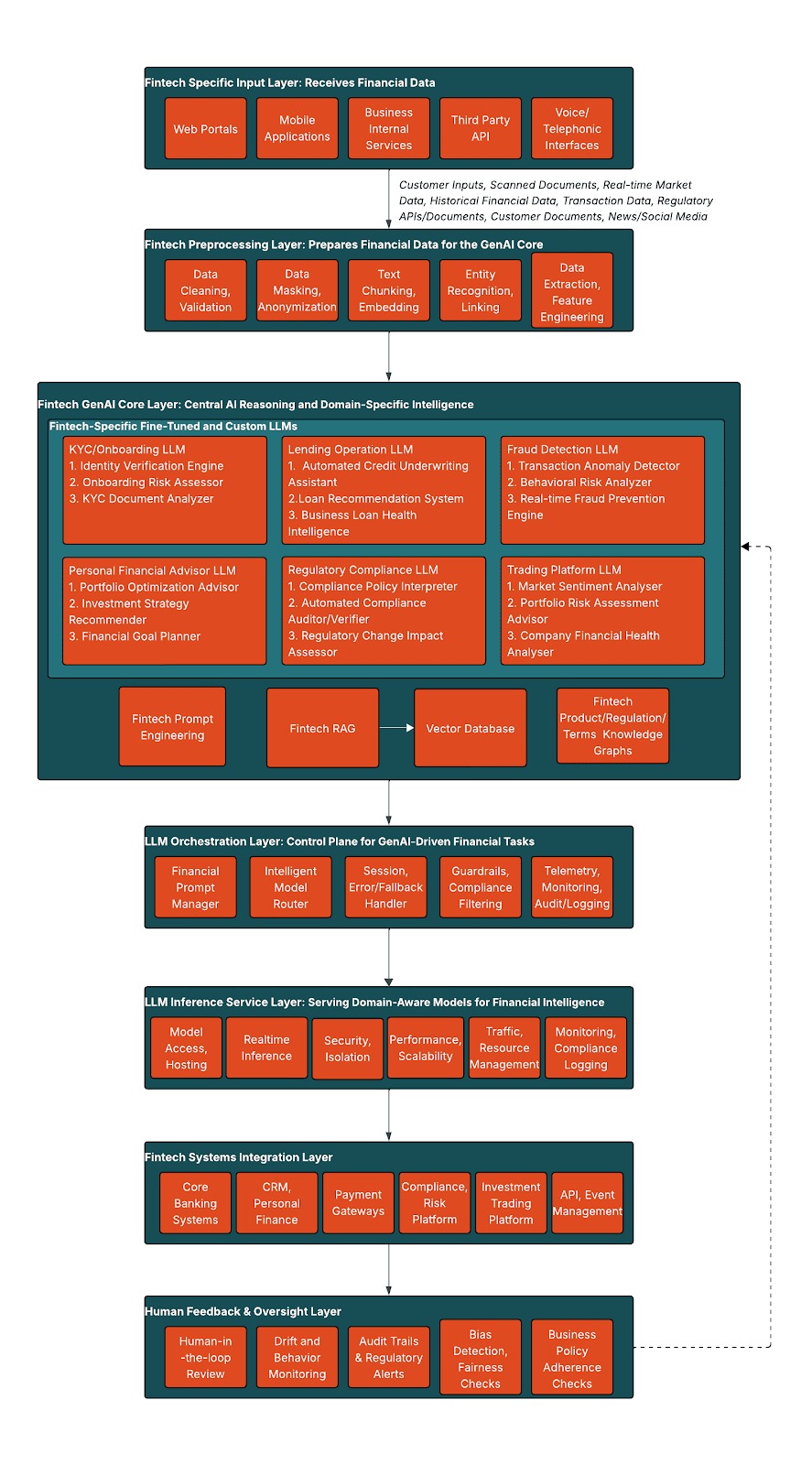

Here are foundational components of a modern GenAI stack tailored for FinTech domain. The overall architecture of the proposed GenAI system is illustrated in Figure 1. To stay ahead in a fast evolving GenAI landscape, this architecture is designed with flexibility in mind featuring modular, model agnostic components and plug-and-play layers that can easily adapt to emerging tools, models and regulatory environments.

1. Fintech Specific Input Layer: Receives Financial Data

The Input Layer is the first point of entry for data into the GenAI system. As shown in Figure 1, this layer captures raw inputs from digital channels used by customers, employees, vendors or internal systems such as core banking, investment, regulation platforms, and backend services. It initiates the GenAI workflow by ingesting both structured and unstructured data ranging from finance documents and chat interactions to transactional logs. Additionally, it brings in external signals including third party APIs, compliance data feeds, financial market events, regulatory bulletins, news articles, and social media.

2. Fintech Pre-processing Layer: Prepares Financial Data for the GenAI Core

This layer converts raw financial inputs into structured, enriched, and privacy compliant formats tailored for GenAI workflows. It addresses the unique challenges of fintech data ranging from banking statements, payment instructions, transaction logs, and credit bureau reports to regulatory disclosures and compliance forms by applying specialized techniques for validation, anonymization, and contextual structuring. Given the precision required in financial operations, the pre-processing layer plays a critical role in minimizing downstream errors and enabling accurate AI driven insights.

- Data Cleaning & Validation: Resolves inconsistencies, fills missing values, and verifies document accuracy especially for sensitive forms like KYC or income proofs.

- Data Masking & Anonymization: Strips or redacts personally identifiable information (PII) to align with data privacy regulations such as GDPR, PCI DSS, and FFIEC.

- Text Chunking & Embedding: Breaks down financial disclosures, T&Cs, or risk reports into vectorized representations for contextual retrieval.

- Entity Recognition & Linking: Identifies financial entities like account numbers, legal entities, transactions, and ties them to internal databases or external registries.

- Feature Engineering & Extraction: Derives structured indicators such as risk flags, spending patterns, or loan eligibility scores from raw statements and documents.

Tools like AWS Textract, Google Document AI, and spaCy are used for OCR, entity recognition, PII redaction, and the parsing of both structured and unstructured financial documents.

3. Fintech GenAI Core Layer: Central AI Reasoning and Domain Specific Intelligence

This layer is the heart of the system, performing deep financial reasoning and decision support using specialized LLMs, RAG, vector databases, and knowledge graphs tailored to core fintech tasks.

- Fintech Specific Fine Tuned and Custom LLMs: Tailored models trained on proprietary financial datasets to enhance task accuracy across fintech use cases.

-

KYC/Onboarding LLM: Verifies identity documents, evaluates onboarding risks, and parses KYC forms using domain aligned prompts and policies.

-

Lending Operation LLM: Automates credit underwriting, suggests personalized loan offers, and evaluates business loan viability based on financial health.

-

Fraud Detection LLM: Detects anomalies in transactions, analyzes behavioral risk, and delivers real time fraud alerts across digital channels.

-

Personal Financial Advisor LLM: Provides goal based investment recommendations, portfolio optimization, and personalized savings plans using user data and market trends.

-

Regulatory Compliance LLM: Interprets compliance policies, audits financial activity, and assesses impact of regulatory changes on business operations.

-

Trading Platform LLM: Analyses market sentiment, evaluates portfolio risk, and delivers company level health insights for trading strategies.

-

- Fintech Prompt Engineering: Designs task specific prompt templates and context injection for automated customer dispute resolution, product recommendation or fraud explanation.

- Fintech RAG (Retrieval Augmented Generation): Augments LLM responses with contextual data such as past decisions, product policies, and regulatory texts.

- Vector Database: Stores semantically indexed financial data like knowledge snippets, prior queries, and FAQs for fast and relevant retrieval.

- Fintech Product/Regulation/Terms Knowledge Graphs: Encodes relationships between financial products, regulatory rules, and policy terms to enable grounded reasoning, traceable outputs, and contextual understanding across use cases.

This layer leverages fine tuned or custom Large Language Models (LLMs) including open source models like LLaMA and BERT adapted for specific FinTech tasks. These models are typically trained using frameworks like PyTorch or TensorFlow in combination with the Hugging Face Transformers library. This layer also incorporates Retrieval Augmented Generation (RAG) using vector databases such as FAISS and Pinecone and applies FinTech specific knowledge graphs to deliver contextualised, auditable, and regulation compliant AI reasoning.

4. LLM Orchestration Layer: Coordinates GenAI Tasks for Financial Precision

The LLM Orchestration Layer serves as the control plane for GenAI workflows within the fintech ecosystem, coordinating how prompts, models, and policies are applied across critical operations. It manages complex decision flows such as real time fraud prevention, portfolio optimization, risk assessment and automated loan document processing by ensuring accurate prompt engineering, dynamic model routing based on sensitivity and SLA, and traceable, policy aligned execution. This layer provides centralized oversight for prompt strategies, fallback logic, and audit logging, making it essential to achieving scalable, secure, and regulation compliant GenAI adoption.

- Prompt Engineering & Context Injection: Builds prompts tailored for regulatory summaries, dispute resolutions, or lending rationales with embedded policy context.

- Model Routing & SLA based Selection: Routes queries to appropriate LLMs (e.g., private for KYC processing, public APIs for customer Q&A) based on task, risk, sensitivity, and latency requirements.

- Multi Model Coordination: Dynamically leverages various models (e.g., Claude for summarization, GPT-4 for document generation, fine tuned in house model for dispute policies).

- Session & Interaction Management: Maintains dialogue state for use cases like credit advisor copilots or onboarding chatbots.

- Fallback Handling & Versioning: Switches models or prompt variants if a response fails to meet financial domain accuracy or compliance thresholds.

- Guardrails & Compliance Filtering: Applies tone, domain, and response boundaries based on financial services regulations (e.g., FINRA, PCI-DSS).

- Telemetry, Auditing, and Usage Analytics: Tracks token level performance, latency, and anomaly alerts critical for audit trails and continuous improvement in regulated environments.

Popular orchestration frameworks such as LangChain and LlamaIndex help coordinate prompt flows, multi model routing, and human in the loop validation in compliance sensitive GenAI deployments.

5. LLM Inference Service Layer: Serving Domain Aware Models for Financial Intelligence

This layer enables secure, real time access to Fintech custom LLMs used in production grade financial applications. It ensures SLA compliance, low latency execution, and seamless integration with GenAI workflows.

- Model Access & Hosting: Provides scalable access to models hosted on platforms like Amazon SageMaker, Google Vertex AI, Azure Machine Learning, and Nvidia Triton with options for isolated or hybrid deployment for regulated workloads.

- Inference Modes: Supports real time (e.g., for customer queries or fraud alerts) and batch processing (e.g., nightly audit reporting or bulk document summarization).

- Security & Isolation: Enforces encryption, API rate limits, workload isolation, and role based access key for PCI-DSS and FFIEC compliance.

- Performance & Scalability: Delivers high throughput, low latency endpoints for use cases like real time customer service chatbots, market data analysis and instant loan eligibility checks

- Traffic & Resource Management: Manages traffic routing, caching, throttling and compute resources to ensure low latency inference, cost efficiency, and service reliability under dynamic financial workloads

- Monitoring & Compliance Logging: Tracks usage metrics and inference reliability while maintaining auditable trails for governance and explainability.

6. Fintech System Integration Layer

This layer embeds GenAI into the operational fabric of fintech systems by enabling seamless integration with mission critical platforms. It ensures that AI generated insights are contextually applied to core banking, compliance, customer servicing, and risk workflows and drives real time automation, regulatory alignment, and data exchange at scale.

- Core Banking & Transaction Systems: Facilitates account analysis, loan automation, and payment risk evaluations through direct integration.

- CRM & Personal Finance Apps: Synchronizes customer insights, intent based messaging, and AI driven recommendations.

- Payment & Settlement Gateways: Aligns GenAI generated decisions (e.g., dispute resolution) with live transaction routing or exception handling.

- Compliance and Risk Platforms: Sends GenAI outputs for review or escalation in fraud detection, transaction monitoring, and KYC operations.

- Investment Trading Systems: Integrates with portfolio management, risk assessment, and execution platforms to support real time decisioning, trade recommendations, and market analytics powered by GenAI insights.

- API & Event Management: Uses platforms like Kafka to enable secure, scalable, real time streaming and bidirectional data integration across fintech systems.

7. Human Feedback and Oversight Layer

In highly regulated financial environments, this layer plays a pivotal role in ensuring that GenAI outputs remain ethical, traceable, compliant and aligned with business policies. It combines human in the loop validation with technical monitoring to uphold accuracy, transparency, and fairness across all AI driven financial workflows.

- Human in the loop Review: Facilitates structured review and approval flows for high risk outputs like loan decisions, compliance summaries, or customer disputes.

- Drift and Behavior Monitoring: Continuously tracks GenAI predictions to detect data drift and maintain relevance over time.

- Bias Detection & Fairness Checks: Identifies and mitigates algorithmic bias, ensuring fair treatment across different demographics.

- Audit Trails & Regulatory Alerts: Logs model behavior, input/output history, and triggers real time alerts for anomalies or policy violations.

- Business Policy Adherence Checks: Checks if GenAI outputs follow internal business rules and financial policies, helping ensure decisions are accurate, compliant, and easy to review during audits.

Strategic Takeaways for Tech Leaders

GenAI is no longer a futuristic addition, it's a foundational force reshaping financial services. This architecture enables organizations to reduce operational costs by 20-40% through intelligent automation, accelerate customer service from hours to seconds, maintain regulatory compliance while scaling AI capabilities, and future proof their technology stack. The question is no longer whether to adopt GenAI, but how quickly and effectively you can integrate it into your core operations. Those who lead with clear strategy and strong technical foundations will steer their institutions toward a faster, smarter, and more resilient future.

Appendix A: Use Case: Credit Risk Assessment – Enabling Smarter Loan Approvals

1. Input Data

- Customer Data: Income, employment status, credit history, assets

- Credit Bureau Reports: Scores, delinquencies, repayment history

- Application Inputs: Loan amount, term, purpose

2. Preprocessing Steps

- OCR & Parsing: Extracts data from uploaded income proofs or bank PDFs

- Feature Engineering: Derives debt to income ratio, credit utilization, risk indicators

- PII Redaction: Protects sensitive data before GenAI processing

3. GenAI Core Processing

- Fine Tuned Lending LLM:

- Evaluates repayment capacity, financial behavior patterns

- Classifies applicant risk (e.g., low, moderate, high)

- RAG Integration:

- Brings in internal underwriting policies or regulatory lending thresholds

- Cites prior approval patterns for similar profiles

4. Orchestration Logic

- Triggered upon loan application submission and LLM assesses credit risk category

- Acceptable risk → offer generation, High risk/edge case → manual underwriter review

- May trigger secondary API checks (e.g., fraud, income validation)

5. Inference Output

- Credit Risk Score, Loan term and amount suggestions

- Approval Recommendation (Approve / Review / Reject)

- Justification summary citing key financial indicators and policies used

6. Integration with Systems

- Output passed to loan origination platform

- Approved → rate/term offer stage, Rejected → rationale logged for audit or appeal

- CRM integration for customer notification and follow up

7. Business Benefits

- Faster Decisioning: Cut assessment time from days to minutes

- Reduced Defaults: Improved accuracy in identifying high risk borrowers

- Explainable AI: Ensures underwriters and auditors understand model logic

- Operational Efficiency: Handles more applications with fewer manual resources

Appendix B: Use Case: Customer Onboarding & KYC Streamlining Identity Verification

1. Input Data

- Customer Inputs: Name, address, date of birth, contact details

- Scanned Documents: Government issued IDs, utility bills, bank statements

- API Feeds: Credit bureaus, identity verification providers

2. Preprocessing Steps

- OCR: Extracts text from scanned documents

- Validation: Checks for format consistency (e.g., DOB, address fields)

- Normalization: Standardizes names, addresses

3. GenAI Core Processing

- Fine Tuned KYC LLM:

- Understands document types and extracts key data

- Matches input vs. extracted vs. API data

- Flags red flags (e.g., mismatches, expired IDs)

- RAG Integration:

- Pulls KYC policy documents or region specific regulations into prompt context

4. Orchestration Logic

- Workflow starts on application submission

- LLM outputs confidence score for identity verification

- High score → auto approval

- Low score or conflict → routed to manual review

- External APIs may be triggered for deeper verification

5. Inference Output

- Identity verification confidence score, List of flagged inconsistencies

- Final recommendation: Approve, Review, or Reject

6. Integration with Systems

- Outputs passed to onboarding system

- Approved customers proceed to account setup

- Rejected or flagged cases enter manual resolution workflow

7. Business Benefits

- Faster Onboarding: Reduces processing time from days to minutes

- Higher Accuracy: Minimizes human error and fraud risk

- Regulatory Compliance: KYC rules are always enforced

- Better Experience: Customers enjoy a seamless digital journey

Opinions expressed by DZone contributors are their own.

Comments