Beyond Netflix: Why Fintech Recommendations Need a Completely Different Playbook

Financial recommendations are high-stakes—unlike a bad movie pick, poor advice can impact long-term goals like retirement. Trust and care are essential.

Join the DZone community and get the full member experience.

Join For FreeLet’s dive into how to create a recommendation system for fintech—hearing for the first time? But don’t worry, I’ll break it down into bite-sized pieces.

The Unique Nature of Financial Recommendations

First off, financial recommendations are a whole different ballgame compared to those you’d get from Netflix or an online store. If Netflix suggests a bad movie, it’s just 90 minutes wasted. But if a fintech app makes a bad investment suggestion, folks could lose their hard-earned savings.

That’s why we’ve gotta be super careful in how we build these systems. Now, here are some big challenges we face:

First up is trust. Users need to believe that the recommendations are actually in their best interest—not just a way for the company to make a buck. It’s a lot more serious than recommending a song or a product.

Then there’s regulatory stuff. Financial services are under strict rules—think FINRA and SEC guidelines. Every recommendation we make has to be defendable and follow the law.

Managing risk is also huge. A risky investment shouldn’t pop up for someone who’s more of a conservative investor—ever.

Also, financial decisions can stick around for a long time. What we suggest today could really affect someone’s ability to retire nicely or buy a house years down the line.

And let’s not forget our diverse crowd. Financial apps hit all sorts of users, from those just starting out with money to seasoned investors—so we can’t use a one-size-fits-all approach.

Key Success Metrics

Now, Let’s discuss success metrics.

Unlike typical recommendation systems that chase clicks, fintech needs to find a balance between user engagement and actual outcomes:

Here’s what to look out for:

Primary metrics include how many new products users adopt, improvements in customer lifetime value, user retention rates, and fewer questions about the recommended products.

For secondary metrics, we can check click-through rates, time spent checking out recommended products, cross-selling success, and user satisfaction scores.

Compliance is crucial too—how complete our audit trails are, if we recommend the right risks, how clear our explanations are, and how many regulatory complaints we get.

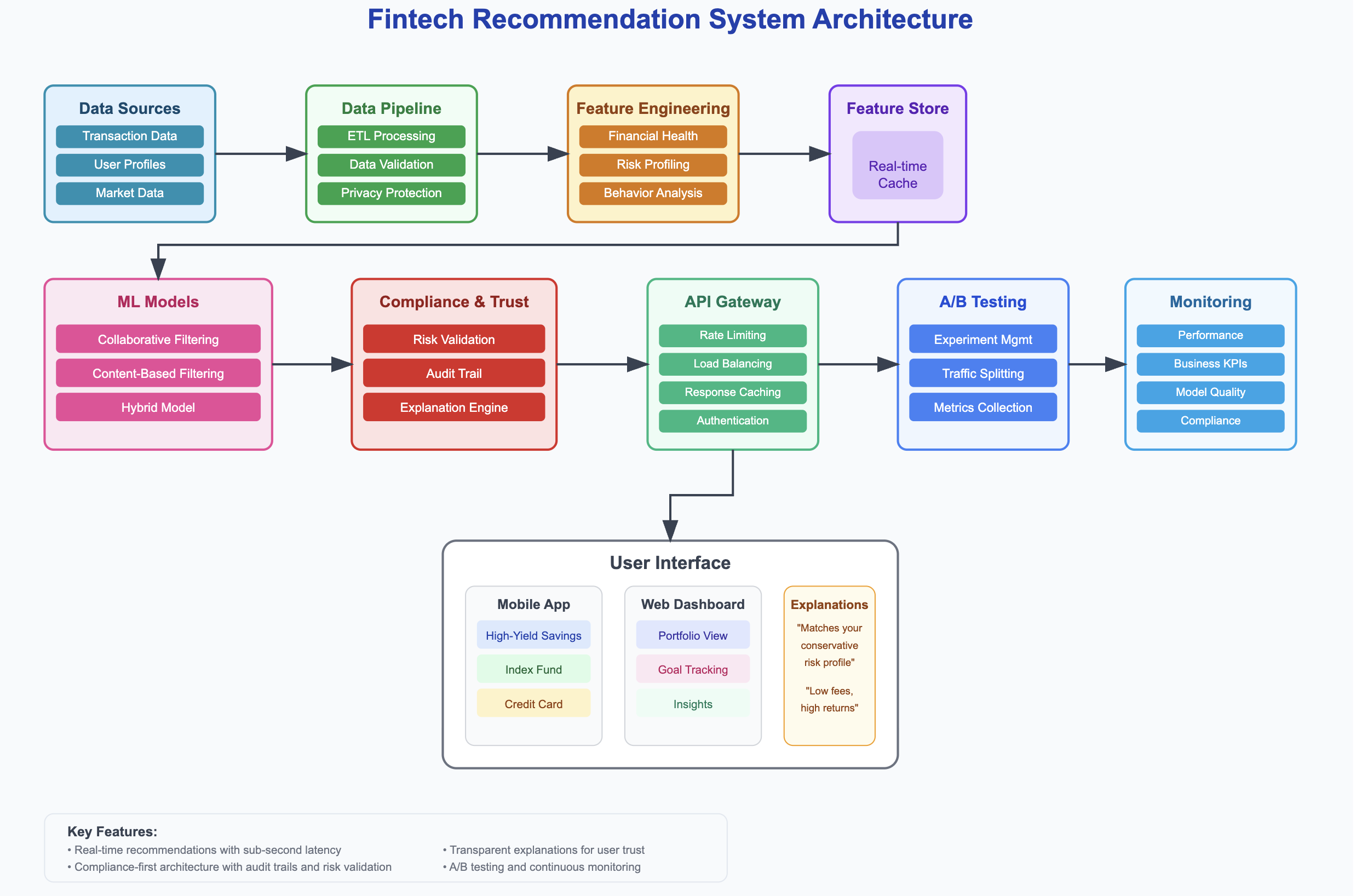

System Architecture and Design

Moving on to system design, we need a solid architecture. A good fintech recommendation system should have different layers to keep things organized:

- Start with the data layer—this is where all the info gets stored and processed. We’re talking about transaction data, user profiles, and market data. It should handle both batch processing for training and real-time processing for live recommendations.

- Then we’ve got the feature engineering layer, turning raw data into cool insights about user behavior, their financial health, and how they handle risk. In finance, we need to consider timing trends and economic situations.

- The model layer comes next, considering all our recommendation models—like collaborative filtering, content-based filtering, and the like. This is where we also support testing and rollouts of new algorithms.

- The API layer is crucial for serving up real-time recommendations super fast. It’s all about keeping users happy and reducing wait times.

- Don’t forget the compliance layer—it ensures everything meets regulations and keeps audit trails intact.

- Lastly, we’ve got the monitoring layer, keeping tabs on performance and making sure everything stays in tip-top shape.

On the design front, security comes first. All user data, especially financial info, needs to be encrypted and access controlled. We’ve also got to ensure our recommendations are clear and understandable for users; this builds trust. If something goes wrong, our system should still work even if one part fails. And we need to keep a complete log of all decisions for audits.

Data Strategy and Feature Engineering

As for data collection, let’s talk about sources. We need transaction data to understand spending habits and transaction history. User profile data helps shape understanding, but we’ve got to be careful with privacy and biases.

Market data—like interest rates and economic indicators—plays a part too. Behavioral data tells us how people use the app. And product performance data gives us insight into what really works.

Now, feature engineering is key. Rather than looking at how much money someone spends, we should analyze patterns—like spending a percentage on housing.

We can create scores that indicate financial stability by looking at savings rates and debt-to-income ratios. For risk, we need to match what users say about their risk tolerance with their actual behaviors. And we need to recognize life stages and adjust recommendations accordingly.

In terms of privacy, we should collect only what we need and anonymize data where possible. Consent management is important too, allowing users to have control over their info.

Recommendation Algorithm Approaches

When it comes to algorithms, collaborative filtering can help us find users who act similarly with their finances for recommendations. But we need to make sure we're focusing on their actual behaviors and not just superficial data.

Content-based filtering is useful for matching user profiles to product traits. It’s a lifesaver for new users or new products without much data.

We can also use hybrid approaches, combining different methods to get the best results. And as we get fancy with deep learning and reinforcement learning, we should keep track of how these affect recommendations.

When we implement this in real-time, we can't afford delays as sub-second response times are a must. We’ll need to cache things smartly to keep user engagement high and performance smooth.

Scaling the architecture means using microservices so different parts can grow independently. We’ll distribute requests smartly and keep an eye on our databases to ensure they’re running as they should.

Once we’re up and running, we need to monitor everything to catch issues early, both in terms of performance and compliance. We’re building trust with users—so clear explanations for why we recommend what we do are vital. We also have to be on top of bias detection and make sure all demographics have fair access.

So there we have it, a wrap-up on building a fintech recommendation system. It’s all about keeping the end-users in mind, because we’re really making a difference in their financial lives. Taking it step by step, being transparent, and ensuring compliance is key to success.

Opinions expressed by DZone contributors are their own.

Comments